As promised/threatened, this is the first issue of Institutional-Grade Options by Benedict Maynard.

It’s the first premium content we’ve offered you lot.

You’re getting the full issue for free today, but they’ll be paywalled in the future.

If you want more like this, consider subscribing (it’s still half off until tomorrow).

What’s Institutional-Grade Options?

We’ve recruited Benedict Maynard, the guy who literally wrote the book on options trade, to produce a fortnightly newsletter that shows you how to trade options intelligently.

No stupid scams. No naked shorts. He’s going to teach you the techniques he refined over 20 years on the trading desk in London.

Each issue will focus on a specific investment thesis and then show you how to build a trade around it.

What’s today’s idea?

We’ve got a strategy to play on two different theses that might become reality in 2024. If either thesis hits, we win. If they both hit, we win big.

Thesis 1 - Reversion to the mean

Over the last twelve months, the vast majority of gains for the S&P 500 was thanks to the so-called Magnificent Seven stocks: Amazon, Apple, Alphabet, Meta, Nvidia, Tesla, and Microsoft.

While the broad index climbed 22% on the year, those seven were up 107%. Together, those seven stocks make up over 30% of the value of the index.

To illustrate the point, compare the TTM returns for two different indices:

SPY - an ETF that tracks the S&P500 Index

RSP - an ETF that tracks the S&P500 Equal Weight Index

It’s not unusual for a small cohort to produce most of an index’s returns. The Pareto Distribution predicts an 80-20 rule for various systems in both natural and human endeavors.

But just like wealth and income, equity returns have become far more concentrated over the last few years.

That’s resulted in the SPY:RSP ratio reaching historically high levels in 2023 that are possibly due for a correction.

Surely the Magnificent Seven will rejoin their less-illustrious brethren at some point?

Thesis 2 - The equities market is due a correction in 2024

Despite a weakening labor market, persistently high rates, and a consumer time bomb, 2023 ended with nine consecutive positive weeks for the S&P 500.

The market is due for a correction.

Further, since 1952, the US markets have performed 10% worse during an election year than the year prior.

There’s a decent shot the S&P will tumble in 2024, and last year’s biggest winners could be first in the queue for a fall.

I’ve asked Ben Maynard, an Alts friend and bloody brilliant human being, to devise a genius strategy to take advantage of this in the lowest-risk way possible.

The Strategy

We’re going to play the SPY and RSP indices off each other using a strategy Ben calls a put switch.

Recall:

The difference between SPY and RSP is their construction methodology. RSP has equal exposure to all S&P 500 stocks, while the Magnificent 7 companies increasingly dominate SPY.

Some definitions if you’re not familiar with options trading:

A put option is a financial contract that gives you the right, but not the obligation, to sell a certain amount of a stock (or other financial assets) at a predetermined price within a specific time period. This can be useful if you expect the stock price to go down because you can sell it at the higher price set in the contract.

A put switch involves buying a put option on one instrument and selling (or shorting) a put option on another instrument. Both put options have the same expiration date of approximately six months, the same notional value of underlying shares, and the same put option delta of around 0.3.

The trade:

We’re going to buy put options on SPY and sell corresponding puts on RSP. Selling the puts on RSP pays for the SPY puts, so the trade is free to execute initially.

The Payoff

There are four general outcomes to this trade based on the direction of the Magnificent 7 stocks and the rest of the S&P 500.

Mag7 Up | S&P 493 Up - both put options expire worthless, so you owe nothing but make nothing. EVEN

Mag7 Up | S&P 493 Down - the purchased SPY put options are worthless; you owe money on the puts you sold. LOSS

Mag7 Down | S&P 493 Up - The purchased SPY puts are in the money; the sold puts on RSP are worthless. GAIN

Mag7 Down | S&P 493 Down - both puts are in the money. Gain or loss depends on which has lost more. This is a profit if SPY has fallen further or a loss if RSP has fallen further, with the magnitudes determined by their relative performance. UNCERTAIN

The two outcomes to worry about, then, are two and four. We get in trouble if RSP loses value AND if it loses more value than SPY.

So, how likely is that?

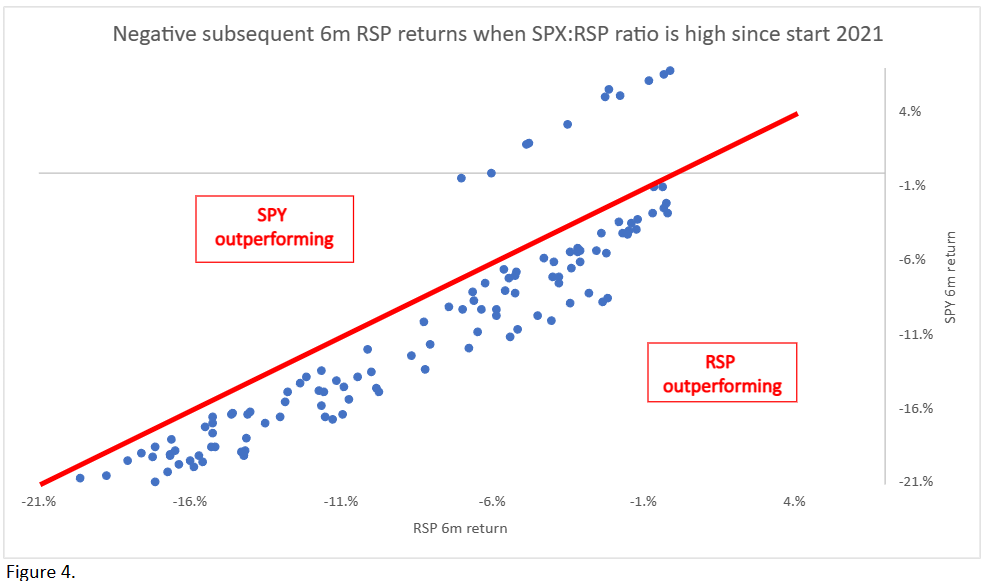

The chart below shows the subsequent six-month return for SPY and RSP since 2021, when

the SPY:RSP ratio is above its average (the chart above with the horizontal orange line).

RSP has declined

You can see that the index reverses a degree of its concentration when the market falls, which feels intuitive when investor positioning has become increasingly focused on large cap tech names since the start of 2023.

In the case of market decline, RSP outperformed SPY 90% of the time.

Again, this makes forward-looking logical sense:

Given the historically extreme S&P500 index concentration, and thus SPY:RSP ratio, and the average forward P/E of 32x for the Magnificent Seven stocks (up from 21x at the start of the year and versus 19x for the S&P500 itself), a recession would undermine the index.

P/E multiples contract during recessions and concentrated speculative exposures get washed out. They also hasten the tendency for equal weighted indices to outperform over time.

A sensitivity analysis of the probable outcomes looks something like this.

Mag7 returns down the left, S&P493 across the top.

Before I walk you through how to build the trade on your own brokerage platform:

If you want more like this, consider subscribing (it’s still half off until tomorrow).

It’s the only way we can keep delivering this 🔥 content.

How to build the trade

Step One - Let’s map it out.

All the price data used in the table above are taken prior to the market opening on 11th January 2024. It's useful to do this prior to the market opening when things are quiet and prices are stable.

Six-month put options equate to roughly a June 21st, 2023 expiration date, and a -0.30 delta is being used (or as close to it as possible).

The ratio for the number of put option contracts to trade is 3 RSP put options sold for each SPY put option bought (i.e. SPY/RSP ETF price = 3.05).

This ensures, crucially, that the notional exposures of the SPY and RSP positions are roughly the same.

This example has a negative $711 notional exposure, which is preferable to a long exposure since this trade works best if SPY falls more in value.

Because the % costs for each are similar and the notional exposures are similar, the trade is almost zero cost because the SPY puts are paid for by selling the RSP puts: in this example, with a small outlay of $27 for the trade since the SPY side is slightly more expensive.

A 3:1 ratio will be used for the rest of this example, but you can increase the multiple (e.g., 9:3, 27:9) depending on your risk tolerance and budget.

STEP 2 - Place the RSP option trade using a LIMIT ORDER

Keep your spreadsheet with the trade map open in case there are market moves while you build the trade.

SPY options are one of the most liquid equity options in the world and can be traded instantaneously within a tight bid / offer spread.

So we want to sell the RSP put first using a limit order. If you are planning a sizable trade, consider breaking it into batches, each with the correct ratio (3:1).

In your broker platform, select RSP as the ticker to trade.

Select the expiration date that is closest to six months into the future - in this case, June 21st, 2024. This will open the screen for tradable put and call options for that expiry as shown below.

Make sure you can see a theoretical price and a delta for the available options.

Because the market wasn’t open when the screenshots were taken, the bid / ask spreads are wide. Bear this in mind as you set your limit order.

On the 'PUTS' side of the screen, select the option that has a -0.30 delta (or close to it) and click on the 'BID' price shown to bring up a SELL trade ticket.

Complete the SELL trade ticket using a LIMIT ORDER as shown above at the theoretical price.

Above, we’re SELLING 3x RSP June 21st expiry 151 strike puts for 2.76.

STEP 3 - Place the SPY trade using a MARKET ORDER

Because SPY is the more liquid option in the trade, it can be done in real-time once the RSP put options have been sold.

Don't hang around, though, because prices do move, and you want to buy these puts as soon as you can after selling the RSP puts to complete the trade.

Firstly, select the same expiration date as the RSP put options that have been sold.

Note that SPY options have a vast array of different expiration dates, so make doubly sure that you have selected the one that EXACTLY matches the RSP option order that has just been executed.

Find the corresponding put option that has the same delta as the RSP put options you have traded, which will be something close to -0.30. Click on the 'ASK' price to create a BUY order ticket.

Make sure the order details are correct and that you are buying the selected put options in sufficient quantity to achieve the desired ratio.

In this example, the order would be to BUY 1x SPY June 21st expiry 460 strike puts at the prevailing market price.

There will be a small amount of slippage as prices move relative to each other once the market opens and during the time between selling the RSP puts and buying the SPY puts, but it is likely to be small.

That’s it. Happy trading!

That’s all for today. Special thanks to Benedict Maynard for this.

Make sure to subscribe if you want more like this.

Cheers,

Wyatt