I’ve got a special issue for you today.

Each Sunday, we explore a different alternative investing topic in our Sunday Edition.

A few weeks ago, we discovered a fascinating trend that almost no one is talking about. It’s called Home Equity Investing

While this is similar to stuff like reverse mortgages and HELOCs, you’ll soon realize this is a very unique market.

This version has been shortened to fit in your email. Read the full issue here.

Today we're exploring a new alternative asset class that has quietly but swiftly materialized: home equity investing.

We first got wind of this market last August while researching our issue on ADU startups and financing.

The under-the radar industry is growing, and the conditions are ripe for it to get big.

I believe that home equity investing may be the single biggest story in real estate almost no one is talking about.

Let's explore 👇

Tap into your home equity without borrowing

As you'll see in this issue, home equity investments (HEIs) provide homeowners a lump sum upfront payment, without loading them up with debt.

Hometap opens up access to this asset class. Fund managers, insurance companies, family offices and accredited individuals can now get a very unique type of exposure to the US residential real estate market.

Home equity investing is a fascinating concept that hasn’t really existed before — at least not in a broad consumer sense.

Now's the time for the industry to shine, and as you'll see in this issue, Hometap is carving an intelligent path forward.

Homeownership has a liquidity problem

Buying a house is the single largest investment most individuals will ever make.

But there’s a surprisingly overlooked financial tradeoff when buying a home. Despite the massive amount of money tied up in real estate, appreciation doesn't directly benefit homeowners until they sell.

A home's value going up looks good on paper, and makes the owners feel all warm and fuzzy. But there’s no real market for selling home equity, so it’s difficult to turn that increased value into actual cash.

Sure, you could sell your home in its entirety. But that’s obviously not ideal if you want to keep living there. Ultimately, sitting on a mountain of appreciation with no way to access it doesn't do you much good.

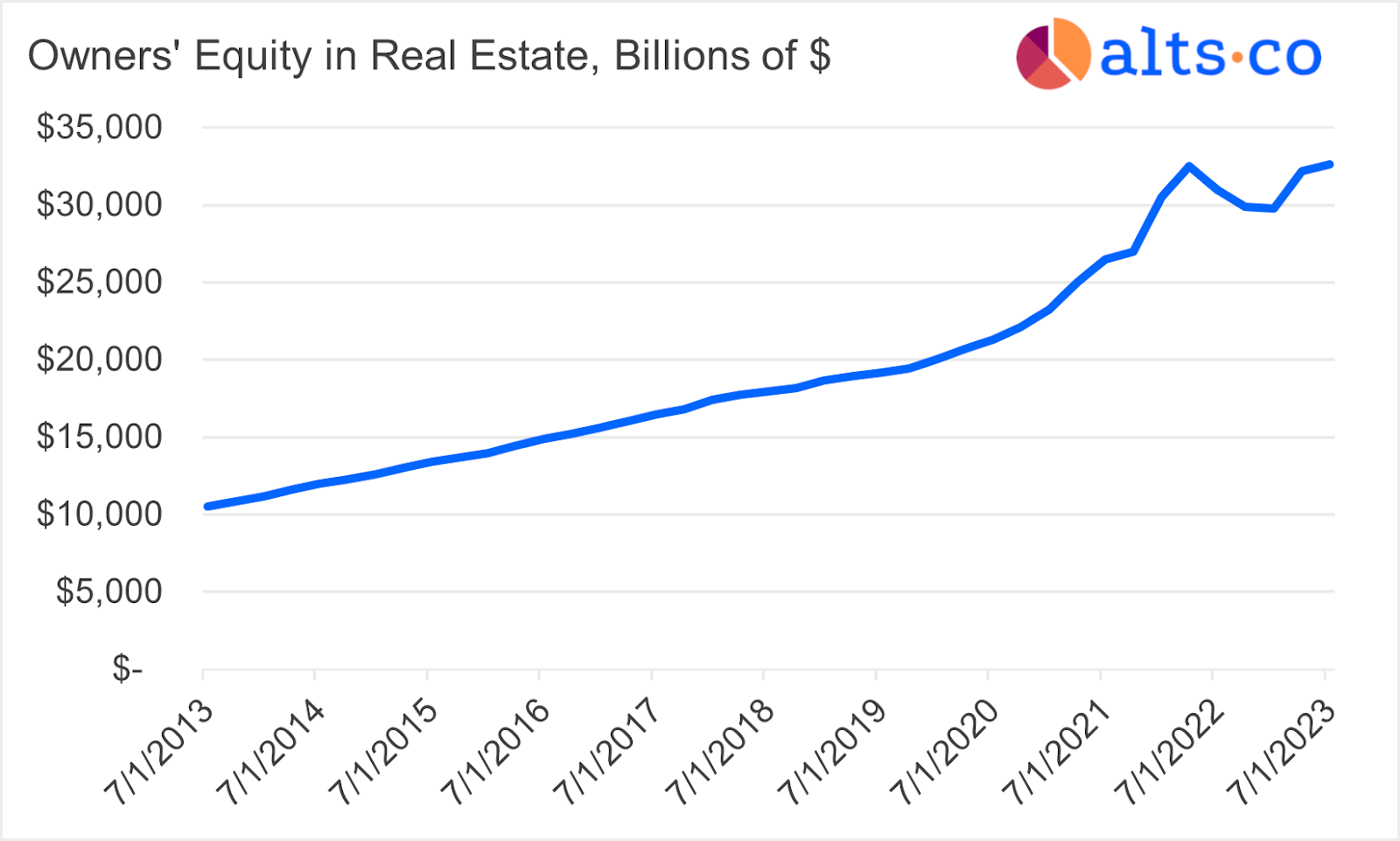

Over the past decade, Americans' home equity wealth has tripled, climbing to over $30 trillion. (For comparison, the total market cap of all companies in the S&P 500 is ~$40 trillion). But what good is equity if you can’t actually access it? Data: FRED

Historically, the workaround for this illiquidity problem has been to borrow against the equity in your home in one of four ways:

Home equity line of credit (HELOCs),

Home equity loans (i.e., second mortgages), or

Doing a cash-out refinance

If you're 62+ years old, you can do a reverse mortgage

While borrowing against your home equity is popular, it does seem absurd that the only way to benefit from your home appreciation is to take on additional debt!

This isn’t just a problem for homeowners — it’s also an issue for investors.

Investors want to access home equity too

As an asset class, residential real estate has some very attractive characteristics:

It has low correlation to traditional stock and bond markets, making them excellent ways to diversify

It's called "real" estate for a reason! It's a real, tangible asset that has become a terrific inflation hedge.

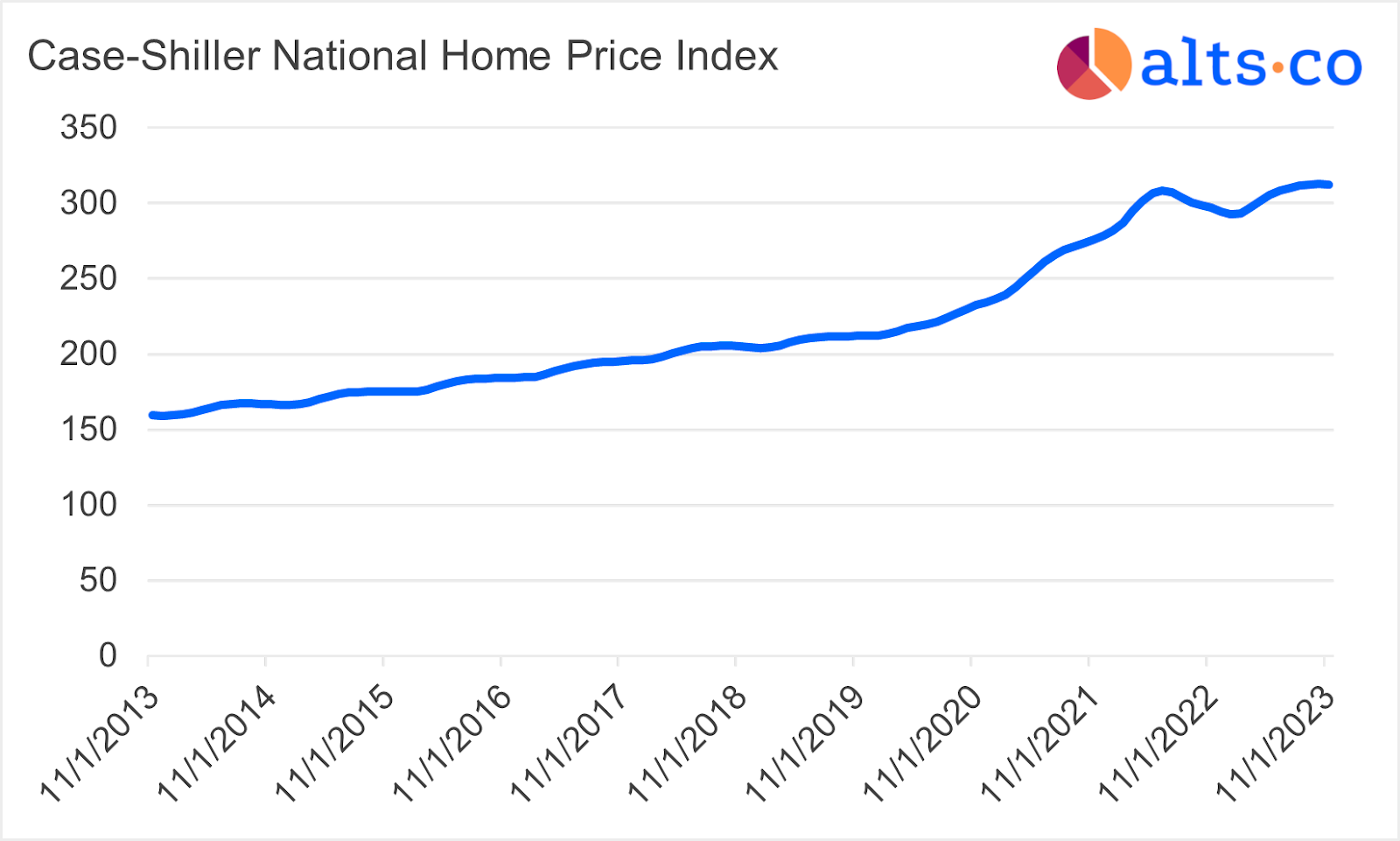

Most importantly, it has shown strong returns. Over the past decade, homes have returned just shy of 7% annually.

Despite a brief interest-rate-induced dip, US homes performed strongly over the past decade, with 7% annual growth and low volatility of 2.4%. Data: FRED

You don't need to invest directly in a home to get exposure to residential real estate. There are all sorts of indirect ways to invest (like REITs, mortgage-backed securities, and fractional real estate platforms.)

But while returns from these options are heavily influenced by home prices, they’re not directly determined by them. There's a value gap at play here.

One fascinating option has quietly but swiftly emerged: home equity investments (HEIs).

How does Home Equity Investing work?

Home equity investments (sometimes called home equity agreements) involve an investor purchasing an ownership stake in someone else’s home.

Example

Let’s start with a simple financial model to explore the mechanics of how HEIs work, (Providers all have unique pricing structures; this is just an example.)

Jane currently owns a home worth $900k. She owes $675k to the bank on a fixed mortgage, so she has $225k in equity.

The local economy booms, and a similar house down the street sells for $1 million. Jane gets her house appraised for $1 million as well. She suddenly has $325k in home equity.

As a result, Jane’s equity falls to $225k, and the investor now has a place in the home's capital stack.

Increased home equity through rising prices can be converted into cash via a home equity investment, which brings an investor into the home's capital stack.

How do investors get paid back?

HEIs turn real estate into something more akin to venture capital than you might expect.

In an HEI, returns are usually predicated on a liquidity event. This can mean selling the home, refinancing the mortgage, or even taking on a new investor.

Let’s say five years go by, and Jane decides to move. She manages to sell her house for $1,400,000.

Since the investor purchased a 10% stake, they’re entitled to $140,000 of the proceeds. That's a 7% annualized return, except it's actually been made liquid. Terrific!

How do HEIs manage downside risk?

HEIs are simple in theory, but more complicated in practice.

First, let's be clear: This market's long-term health depends upon house prices rising indefinitely. An extended period of home prices falling or even stagnating (like we saw in '08) could bring the industry to its knees.

This risk needs to be baked in. (We'll show you how they do this below.)

Second, to deploy HEIs in the real world you need to make all sorts of micro-adjustments.

In our example above, we assumed the investor who purchased a 10% stake would also receive 10% of the proceeds when the house sells.

But there’s no reason things need to be structured this evenly!

As an equity investor, you need to consider the downside risk (falling or stagnant home prices) to a larger degree than you would if you were lending money through, say, a HELOC.

And the way investors protect their downside is to require a higher percentage of the home value at the time of sale than what they originally invested.

For instance, Hometap typically makes an investment equal to 10% of a home’s value (although this can sometimes be higher).

But on the way out, their ownership share rises to 15% or more.

In fact, the final % share Hometap owns depends on when you sell, and whether your home has gone up or down in value.

Hometap’s ownership share at the end of the investment tends to be greater than what they initially invested — with some additional incentive for homeowners to settle the deal early.

This varying ownership share hints at another crucial feature of HEIs in practice: the liquidity clock.

2) By imposing a time limit

In our example, the return was triggered by the sale of the home — a very normal liquidity event.

But what if the house doesn't sell? What if the owner is a retired individual with no plans to ever move or refinance?

HEI investors don’t want to wait around forever to be repaid. So they usually implement a liquidity clock — a timer that starts ticking down the moment an investment is made.

Once that clock runs out (with Hometap, it's 10 years), homeowners must repay investors, whether through savings, selling their home, or borrowing against it.

Conflicts over control & decision-making

HEI investors play an odd role in this game.

While they’re not owners in the traditional sense, they’re also not as hands-off as lenders might be.

This middle ground results in some complex conflicts over who gets to make key property decisions.

Sale price conflicts. If the house goes on sale, the investor is obviously incentivized to sell for a higher price. But the homeowner might want to sell quickly, even at a loss. Who has the final say?

Renovations. If a homeowner materially improves the home's value on their own dime, should the investor have the right to profit from those renovations? Even if they had nothing to do with financing them? What if a homeowner does the repairs by themselves?

Payment waterfall. Where do investors sit in the repayment flow — especially if there are already multiple loans on the same property?

Home equity investors are co-owners of a home. But should they have the right to help make critical decisions about the property?

Hometap states:

As long as you’re paying your mortgages, taxes, and insurance, you do not need to loop them in on decisions about your home (except for decisions relating to financing).

Hometap does not profit from the value added/appreciation earned from renovations (as determined by an appraiser).

They also do not dictate the sale price (except in that it must at least approximate market value).

But not all investors are likely to be so lenient, and the fine print of some HEI agreements may be more dubious.

Are HEIs a good deal for homeowners?

It's compelling for homeowners

It’s easy to see how HEIs could be a terrific opportunity for homeowners who want some extra cash. Finally, they can realize value from their home without taking on debt or monthly payments.

Remember, an HEI is only repaid when the home is sold (or at the end of a set term.)

You’re not even selling current equity in your home like you are with a reverse mortgage. Instead, you’re selling a portion of your home’s future value in exchange for a lump-sum payment today.

Oh, and it’s not dependent on a high credit score, household income, or debt-to-income ratios! What matters is the home and its potential future value.

For homeowners, HEIs can be extremely compelling, because all the risk falls on the lender!

But there's a drawback

But HEI does have one major drawback compared with traditional debt: It's very difficult to know exactly how much you’re paying.

Understanding the cost of something like a second mortgage is fairly simple. You’re charged a fixed rate of interest (usually) on a set amount of money, paid back in regular installments.

But HEIs come with a lot more uncertainty.

You don’t know exactly when you’ll be paying back the investor or how much you’ll owe.

To illustrate this, I took Hometap’s terms and calculated a very important metric: the effective annualized interest rate.

This is the rate homeowner would end up paying once the investment is repaid, depending on how long it took to repay, and how much the home rose (or fell) in value.

Suppose you received a home equity investment of $100k cash on a $1 million home.

Your home appreciates 2% per year, for 6 years. Reasonable.

The value grows to $1,126,162. Great.

When you repay the HEI, you’d owe Hometap $200,457 (or 17.8% of the home's value)

This would give you an effective annualized interest rate of about 12.3%.

Now, whether 12.3% is better or worse than a rate you could get elsewhere depends on your credit score, your level of home equity, and a whole bunch of other factors.

But the larger point is that it's not obvious from the start what the true cost of an HEI will actually end up being.

It feels weird to think about an "interest rate" when you aren't actually taking on any debt! But this is the right way to consider what you're really paying.

This chart uses Hometap's terms to show how changes in home value affect the effective annualized interest rate. Chart assumes a 10% upfront investment where origination fees are not included.

What’s more, many HEIs come with additional origination fees in the range of 2-5% of the total investment (Hometap does 3%). This is roughly in line with the closing costs of mortgages or HELOCs.

On average, homeowners can expect financing costs of HEIs to be higher than borrowing money.

But the lack of needing to take on debt cannot be stressed enough. There are no repayments.

HEI effective interest rates may be higher, but the ability to get a big lump of cash today without worrying about monthly payments will always be compelling.

There's no other market out there providing this.

Are HEIs a good deal for investors?

The biggest risk in this market is a sustained real estate downturn.

If home prices fall, there’s a risk of poor returns. People who take HEIs tend to have a higher risk profile to begin with. And if you have a sustained frozen market where inventory barely budges (again, like we had in '08) the industry could get ugly..

But given the creative ways HEIs are structured, home prices would have to fall for a very long period of time for investors to lose money.

Referring back to the interest rate chart, investors would only lose money if home prices fell 5% annually for 8 years or more. This would be a more severe drop than we had when the US housing bubble popped.

In a game like this there is always prepayment risk. This occurs when a homeowner settles their HEI early, causing investors to potentially have to redeploy capital at a less attractive rate.

But remember, the earlier the homeowner pays back the HEI, the higher Hometap's cut of the value, The payment structure itself disincentivizes early repayment. So this risk can be mitigated as well.

First-mover advantage

There's a strong first-mover advantage going on in HEIs right now.

This asset class is just getting off the ground, and there just aren’t that many HEI providers. So there's ton of alpha still left to be harvested (especially compared to mortgages, which are offered by basically every bank in country.)

As a result, HEIs have a higher Sharpe ratio (a measure of risk-adjusted return) higher than almost any other asset class.

So far, HEIs have a very strong Sharpe ratio. While this is not a perfect measure of risk-adjusted return, it does indicate the potentially higher returns and lower volatility of this new asset class. Image: Hometap

A (nearly) perfect storm for growth

The home equity investing market has only truly started to take off in the past few years, which makes it challenging to get broad data.

But we could be seeing a perfect storm for growth in this market

Mortgage rates. In the past two years, average 30-year mortgage rates have jumped from about 2.5% to close to 7%. This means it's super expensive it is to borrow against your home equity right now.

Tappable home equity (the amount homeowners can access while still having 20% equity) is $11.5 trillion, and sitting near record highs.

Home sales have fallen to a 13-year low, meaning plenty of homeowners are going to be looking for a different way to convert their equity into cash.

The only thing making this market less compelling is the chance that interest rates are expected by many to come down in 2024.

But conjecture is not fact. And even if rates begin systematically lowering, this will happen slowly, giving this heading up market plenty more time to simmer.

How to invest in HEIs

Despite the market’s growth, there still aren’t many investment platforms offering HEIs.

You need to work directly with companies operating in this space.

Hometap

They are one of the few companies in this space that reliably originate HEI opportunities which add value both for homeowners and investors.

This market is all about balance. To date, balancing both sides of the market has proven successful:

10,000+ home equity investments made.

~$1.5 billion in committed capital from investors (Bain Capital Credit, Delaware Life, and others)

And a 19% (!) historical internal rate of return with a five-year track record.

Plus, they’re vetted and backed by some of the top VCs in the world, including General Catalyst.

And you’re not just investing in HEIs piecemeal here: Hometap offers investors access to asset funds, which are designed to be diversified portfolios of HEIs.

Closing thoughts

I've been thinking the HEI market since mid-2023, and l don't quite understand how it's not bigger.

It has seen a lot of growth in the past few years, but still seems to fly under-the-radar. Compared to how much the media used to discuss reverse mortgages back in the 2000s, chatter about HEIs seems tepid.

Perhaps I'm missing something else on the risk side? Perhaps borrowers aren't as desperate for expendable cash as I'd thought? Perhaps it's about to take off? The truth is probably somewhere in the middle.

In particular, I think offerings for individual investors will expand, creating more accessible ways to get exposure here:

Public products, like a mutual fund, ETF, or dedicated HEI REIT would lower minimums and allow for more liquidity.

Online investment platforms will probably tart offering HEI opportunities. (I couldn’t find a single one that does this today – email us if you know of any!)

A secondary market for buying fractions of home equity shares is unlikely to happen for some time.

When it does, it'll likely be through tokenization.

However the market develops, one thing’s for sure: HEIs are going to continue to grow, and this is definitely an alternative asset class that investors would be wise to pay attention to. 🏡

That's all for today.

Reply with comments. We read everything.

See you next time.