Stocks & Income is proudly brought to you by Alts, the world’s leading platform for exploring and investing in alternative assets.

Each Sunday, we publish a special, in-depth issue about a different alternative investing market.

Today’s issue is on international stocks.

Enjoy!

Welcome to the Alts Sunday Edition 👋 Hope you enjoyed last week's issue on surging coffee futures.

We are living in some very interesting times for investing.

Since Trump took office, trade war fears have caused the S&P 500 to fall 7%, consumer sentiment has dropped 11%, bitcoin is down 22%, and volatility has surged as investors grapple with growing uncertainty about the future.

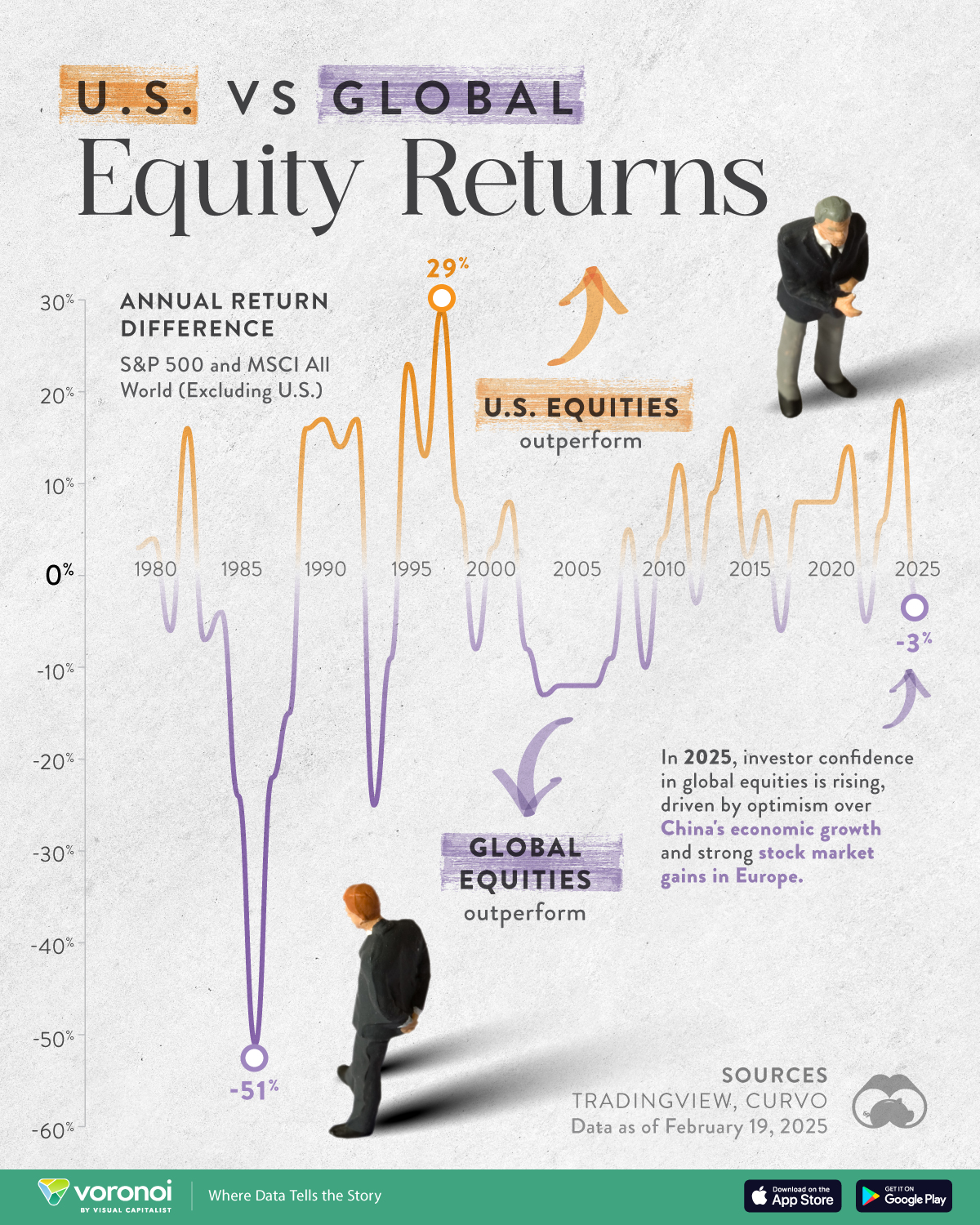

Here at Alts, our goal is to shine a light on under-explored assets, companies, and markets. Over the past decade, US equities have dominated financial media — and for good reason. They generally outperform international stocks.

But right now, international stocks are outperforming the S&P 500.

There are early signs that we may be seeing the start of a significant rotation out of US stocks and into international equities.

The fact is that many of the most under-discussed investing opportunities are found in other countries. So today, we're going to look at a few of these.

And in the spirit of staying alternative, we'll look at two stocks with high dividends. Because let’s face it: dividends are another under-discussed area of investing.

Let's go 👇

This issue was co-authored by Max, the founder of MaxDividends.com — an entrepreneur, father of three, and private stock investor. He focuses on high-yield dividend growth stocks to build a reliable income stream, sharing his journey and strategies through his Substack. This is his first guest issue with Alts.

Why invest in dividend stocks?

It’s easy to forget that dividends are one of the cornerstones of capitalism — a direct link between a corporate profits and shareholders.

Before buybacks, before meme stocks, before the era of zero interest rates and tech-fueled hypergrowth, companies rewarded investors the old-fashioned way: by literally sharing the wealth.

Dividends represent capitalism in its purest form: A business earns a profit, and returns a portion of that profit to the people who backed it.

It’s unsexy, but predictable — and that predictability makes dividend stocks a powerful tool for long-term investors, especially during economic downturns. (Yes dividends can be lowered and raised, but they don't move as rapidly as stock prices!)

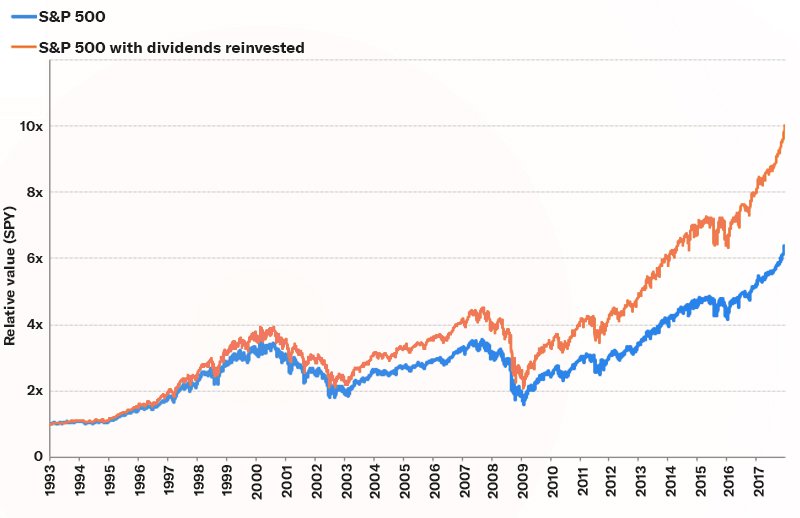

Stock price charts are misleading for investors, because they don't factor in reinvested dividends.

Dividends tend to be higher outside the US

Yet today, dividend stocks are often overlooked by American investors. And one reason could be that international companies tend to offer higher yields than US-listed companies.

While American firms typically prioritize share buybacks and stock price appreciation, dividends play a much larger role in shareholder returns across Europe, Australia, and parts of Asia.

"US dividend yields are generally lower than those of non-US markets, particularly developed markets like Europe and Australia. This is partly because US companies favor share buybacks as a means of returning capital to shareholders." — J.P. Morgan Asset Management, 2023 Guide to the Markets

Australia in particular is known for high dividend payouts — supported by a tax system that actively incentivizes profit distribution to shareholders, through something known as franking credits.

When an Australian company distributes profits to shareholders, it often includes a tax credit for the corporate tax that has already been paid on those profits. Shareholders use these to offset their own personal income tax. This is a huge reason why Australian dividend yields tend to be higher than in the US — and why dividend investing is such a core part of Aussie portfolios.

Later on in this issue, I'll tell you about one Aussie company in particular who has strong performance, high dividends, and franking credits.

In the meantime, Stefan is in Scandinavia this month. So let's look at two Nordic companies that aren't on most investors' radar.

Assa Abloy 🇸🇪

What is Assa Abloy?

Assa Abloy is a global leader specializing in physical and digital access control.

Think:

Automatic doors, entrance systems, and door closers

Locks and padlocks (residential and commercial)

Smart locks and biometric systems

Based in Stockholm, Sweden, they operate in over 70 countries, with a massive portfolio of over 200 brands, including well-known names:

HID Global (leader in secure identity)

Mul-T-Lock, Medeco, EM, Traka, and more

Company history

ABLOY was founded in 1907 when a young mechanic from Helsinki, Emil Henriksson, invented a unique locking mechanism based on rotating locking discs, which became the foundation for all ABLOY locks.

In 1919, this invention was patented, and the company Ab Låsfabriken was established in Finland. 75 years later, the company merged with its big Swedish competitor, ASSA.

And that's how we got Assa Abloy.

Why invest in Assa Abloy?

Assa Abloy is a proven dividend champion; an attractive option for long-term investors seeking reliable returns.

Global leader: #1 or #2 position in most of their markets

Quiet compounder: Not flashy, but consistent returns over time

Plays into major long-term trends: urbanization, IoT, smart homes, and security tech

Not a hypergrowth stock, but a solid, well-run company with steady cash flows

Often overlooked in the US, but considered a Swedish blue chip stock

Dividends

Assa Abloy pays a reliable annual dividend, though not extremely high — yield tends to hover around 1.64% — but it's consistent, supported by solid free cash flow, and getting bigger each year.

10-year dividend yield on cost (Max Ratio): 4.07%

5-year dividend growth rate: 54%

Consecutive years of dividend payouts: 14+ years

5-year average payout ratio: 40%

In the world of dividend investing, there is always a balance between between rewarding shareholders, and retaining earnings for reinvestment. Assa Abloy takes a balanced approach, and has had 14 straight years of increasing dividends.

They’ve also weathered downturns well, benefiting from:

Global demand for security (defensive sector)

Recurring revenue in software/access control

Strong market share in both emerging and developed markets

The Current Payout Ratio is 38.4%, which is lower than the 10-year average. That dramatic spike a decade ago may have been caused by a temporary dip in earnings, or a one-off accounting event. After the spike, the payout ratio normalized into a healthy range. Under 50% is considered sustainable.

Financials

Not only are Assa's dividends rising, but revenue is rising as well.

Growth

Assa is forecast to grow earnings by 9.3% and revenue by 6% per year.

Earnings per share are expected to grow by 9.3% per annum. Return on equity is forecast to be 15.5% in 3 years.

Risks

Construction & real estate exposure. When construction slows (due to high interest rates, inflation, or weak economies), demand for doors, locks, and access systems tends to dip.

Valuation risk: Assa trades at a premium to traditional industrial or building products companies. But in a downturn, that premium can compress quickly. It’s a "steady compounder," not a cheap deep value play.

Geopolitical + currency risk. Assa Abloy operates in 70+ countries, which is great for diversification — but also exposes the company to currency volatility (SEK/USD, SEK/EUR, etc), and import/export tariffs.

Editor's note: We've been polling readers of our Stocks & Income newsletter about their international investing habits.

Results show many readers are curious about it, and most are investing through region-specific ETFs, like the iShares MSCI All Country World Index ex-US ETF, $ACWX ( ▼ 2.28% ), which is up 8.2% this year, outpacing the S&P 500.

Coloplast A/S 🇩🇰

What is Coloplast?

Think:

Continence care (catheters, urine bags)

Wound and skin care products

Urology and surgical products

Ostomy care, which is Coloplast's largest business unit

Ostomy Care products bring in 9.5 billion DKK in revenue ($1.3B USD) — about 7% of Coloplast’s total income.

This is stuff many people don’t like to talk about — but they're essential for maintaining a high quality of life. Coloplast focuses on discreet, user-friendly products for people living with chronic conditions.

This specialization gives it a strong market position, pricing power, and consistent demand, making it a resilient choice in any economic climate.

Company history

Coloplast was founded in 1957 by Elise Sørensen, a Danish nurse whose sister had undergone ostomy surgery. Elise wanted to create a product that would allow her sister to live a normal life again — and the world’s first adhesive ostomy bag was born.

That simple idea turned into a global leader in intimate healthcare, now employing over 14,000 people and serving millions worldwide.

Coloplast A/S generates the majority of its revenue in Europe. The company focuses on developed markets like Germany, France, the UK, and its home country, Denmark.

Why invest in Coloplast?

Coloplast is one of the most consistent dividend payers in Europe, and is considered a Dividend Aristocrat.

With 25+ years of consecutive dividend increases, Dividend Aristocrats have a proven track record of not only maintaining but consistently increasing their dividends, often outperforming the broader market.

Coloplast delivers steady revenue and earnings growth, even through downturns. It's an attractive option for investors seeking stable income from the defensive healthcare sector:

Defensive industry: Demand is tied to aging populations and chronic care needs

Global leader in niche but essential healthcare segments

High margins and strong ROIC: Coloplast is known for operational excellence

Track record of innovation, with a user-first design approach

Dividends

Projected 10-year dividend yield on cost (Max Ratio): 4.81% (reflecting strong potential for long-term dividend returns)

5-year dividend growth: 29%

Consecutive dividend payments: 30 years

5-year average payout ratio: 90% (demonstrating the company’s commitment to returning value to shareholders)

Financials

Coloplast has a strong history of increasing revenue, and stable profit:

Gross margin: ~70%

Operating margin: ~30%

Return on equity: ~45% (among the highest in Europe)

Growth

The company expects organic growth of 8-9% and an EBIT margin (before special items) of about 28% for the 2024/25 financial year, with no changes to its previous forecast.

Coloplast's current Dividend Yield of 2.75% is higher than the 10 year average.

However, the Payout Ratio of 93.8% is lower than the 10-year average, meaning the company is now paying out a smaller portion of its earnings as dividends compared to the past.

A lower payout ratio means the company is keeping more of its profits to reinvest in the business or build up cash reserves, which can support long-term growth.

In contrast, a higher payout ratio in the past could have meant the company was stretching itself thin to pay dividends. So this could be a sign of more sustainable dividend policies.

The payout ratio is still higher than a typical industrial stock — but that’s normal in the healthcare space, especially for mature companies with limited reinvestment needs.

Coloplast operates with minimal debt, high margins, and reliable cash flow — all of which support a very sustainable dividend policy.

Risks

Regulatory risk: As a medical device maker, Coloplast is exposed to changing healthcare laws and reimbursement policies, especially in the US and EU.

Currency risk: Revenue comes from 140+ countries — fluctuations in EUR, USD, and emerging market currencies can impact earnings.

Niche market saturation: Coloplast is dominant in a few very specific markets. While that’s great for margins, it limits the scope of potential explosive growth.

The Taiwan Semiconductor Manufacturing Company beat out LVMH, Novo Nordisk, and Mercado Libre as the international stock readers most want to hold:

Okay, that’s all we can fit in one email.

Disclosures

This issue was co-written by Max Dividends. Editing was done by Stefan von Imhof.

Neither Alts nor Altea has any current holdings in any companies mentioned in this issue

This issue was sponsored by Gemini

This issue contains affiliate links to TradingView. If you sign up, we get a few bucks.